Dr. Stace Sirmans

Profile

I joined the finance department in the Harbert College of Business at Auburn University in the fall of 2018. I received my Ph.D. in Finance from the University of Florida. My research interests include the areas of AI in finance and real estate, investments, credit, real estate, international finance, and sovereign risk.→stacesirmans@auburn.edu

→Download CV

→Google Scholar

→Online Financial Calculator

Projects

Corbis

Answers you can trace back to the source

Evidence-grounded AI for finance, real estate, and economics. It answers research questions from peer-reviewed work and attaches an inspectable citation to every claim, so the evidence can be checked rather than taken on faith.

REIT Factors

A transparent factor library for REIT research

An open, replicable factor library for real estate research, built from our 2025 working paper. It publishes six REIT return factors and their monthly return series, so other researchers can reproduce and extend the analysis.

The Price of Intelligence

A hedonic price index for AI capability

A public, labeled family of price series for public API inference. Over the same market and the same 20 snapshots, posted prices of continuing models rise while the price of a fixed level of benchmarked capability falls, so the measured direction of price change depends on what is held fixed.

Journal Publications

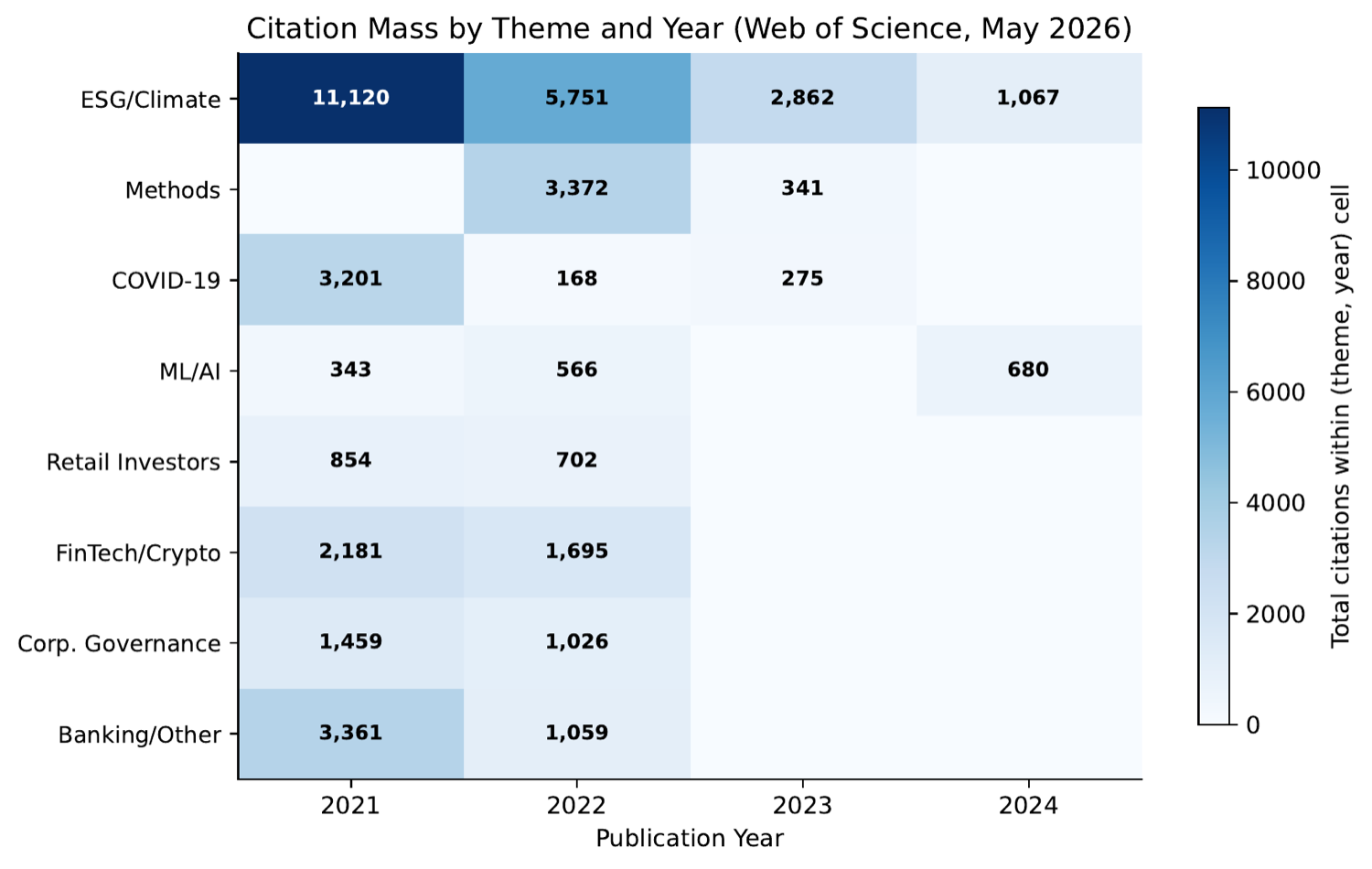

(2026) “Frontiers and Foundations: Insights from the Most-Cited Finance Papers, 2021–2026” (with Cayman Seagraves), The Financial Review, forthcoming.

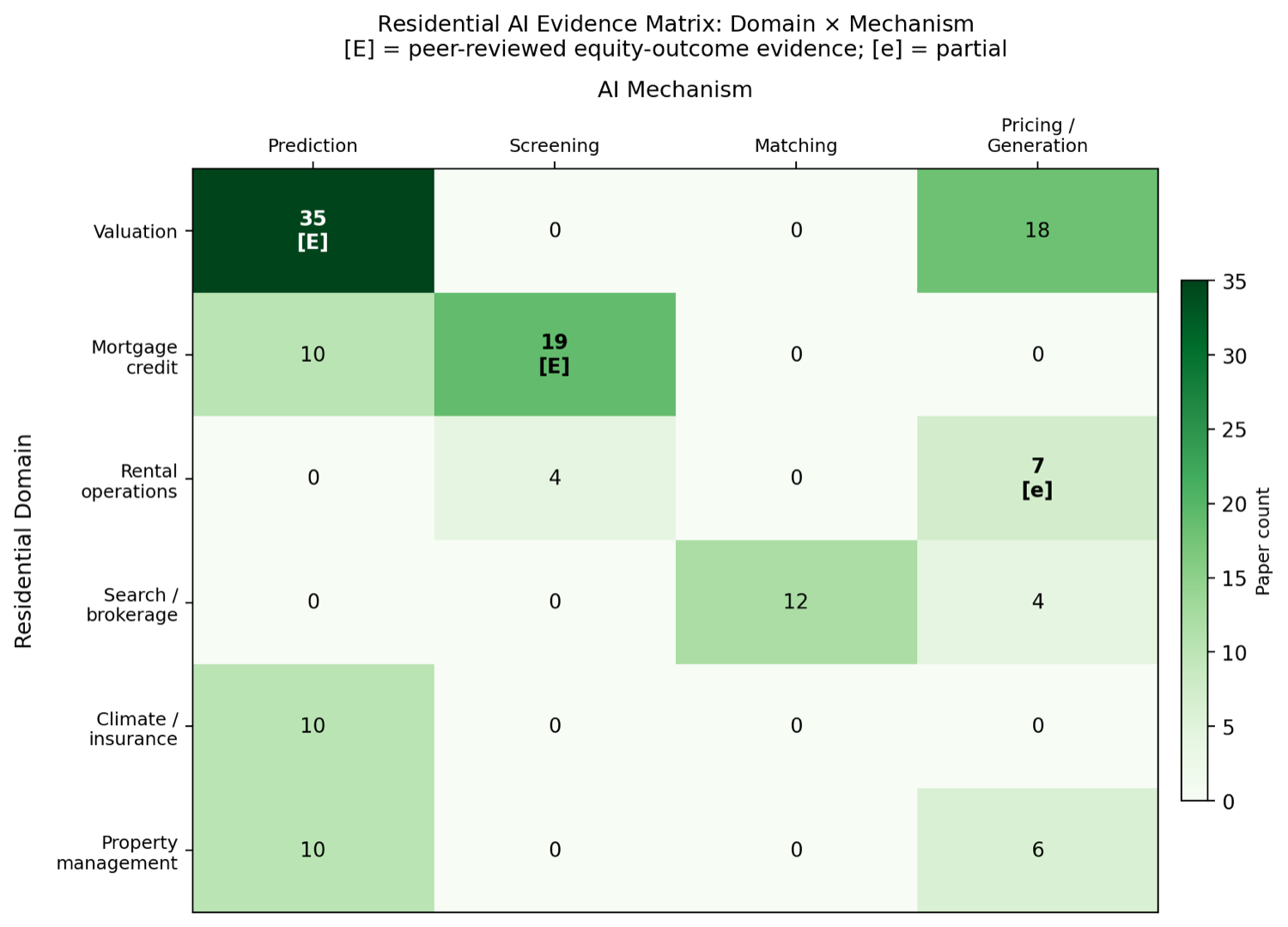

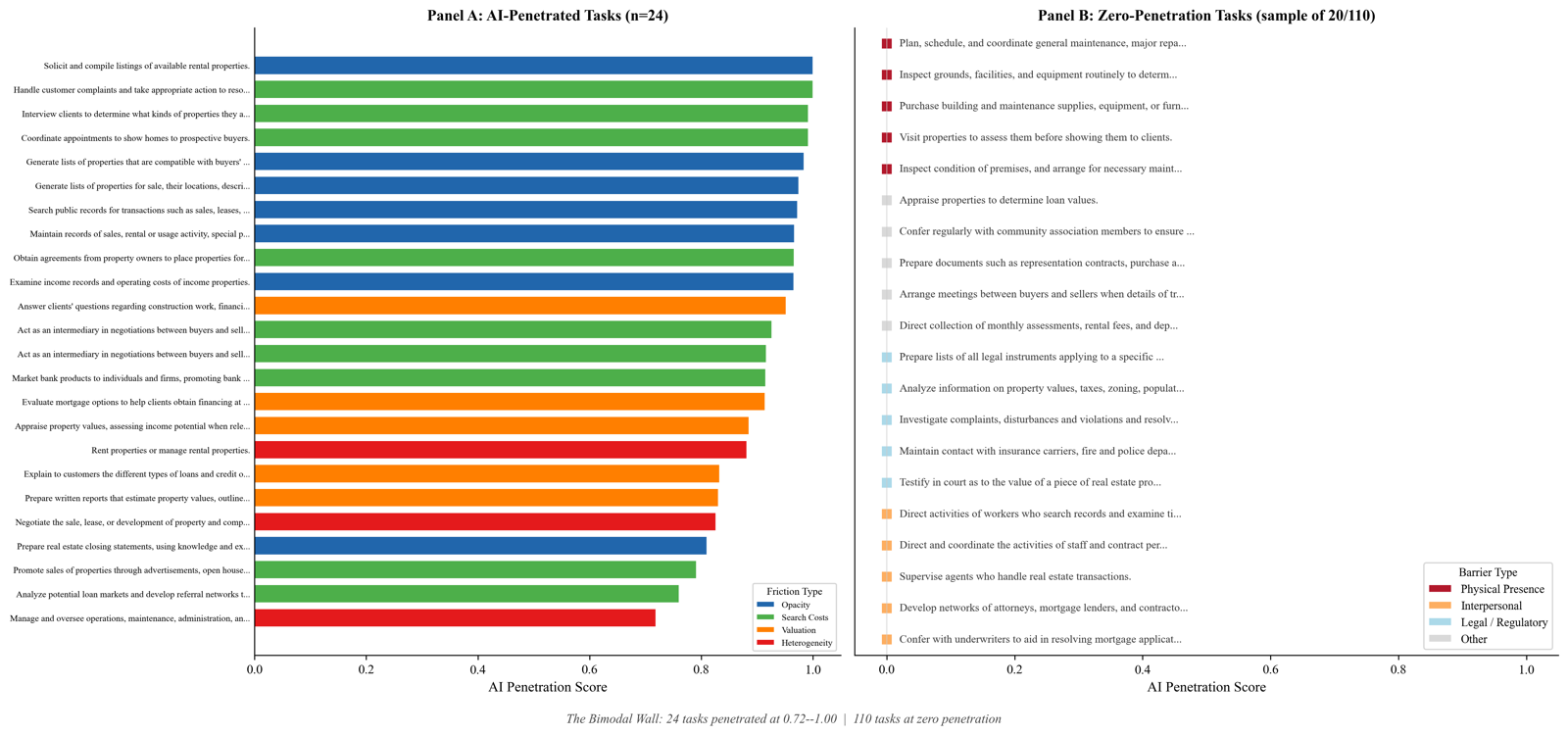

Paper overview(2026) “The Agentic Frontier: Artificial Intelligence in Commercial Real Estate” (with Cayman Seagraves and Michael Seiler), Journal of Real Estate Research, forthcoming.

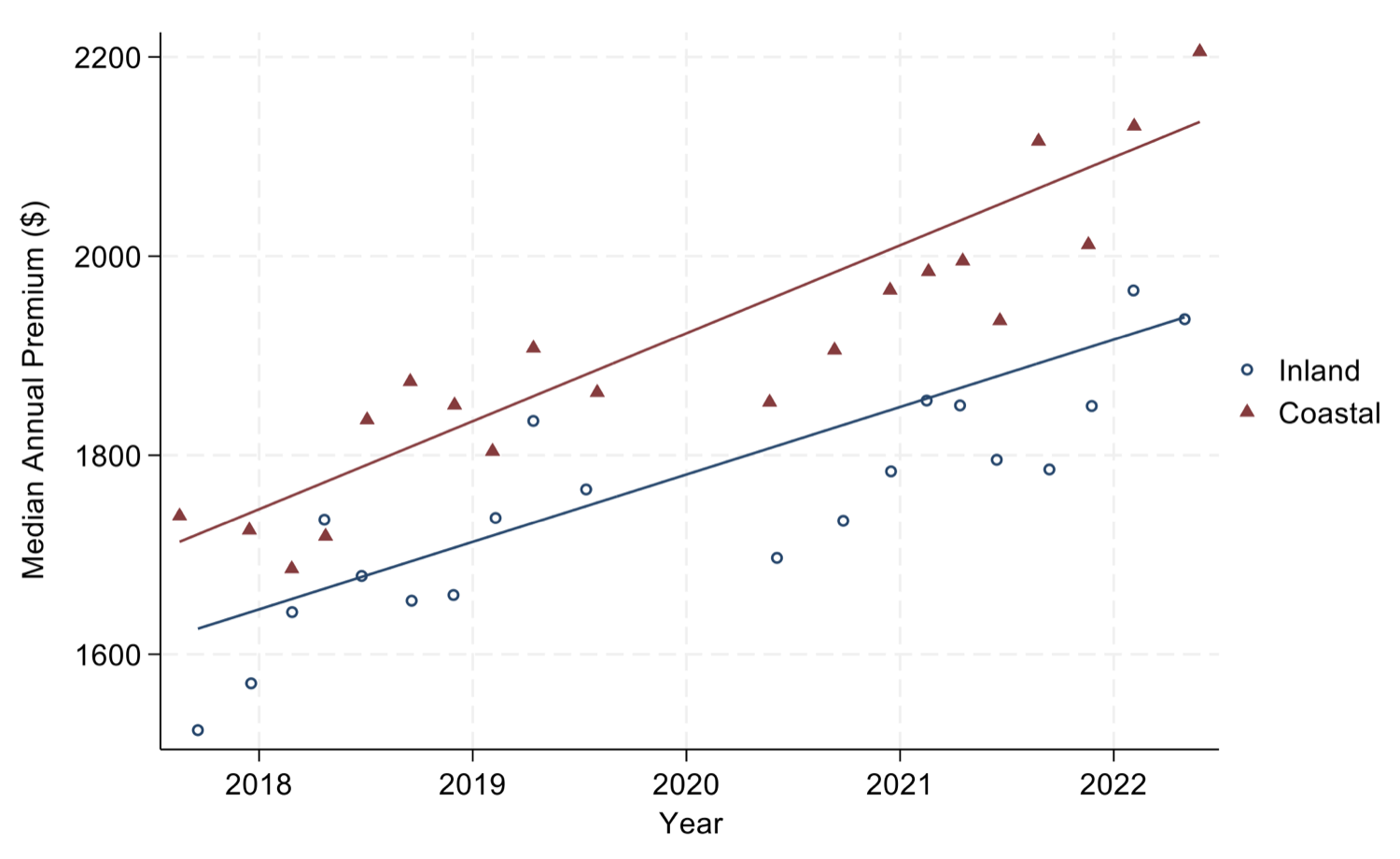

Paper overview(2025) “Climate Change Opinions, Disaster Risk, and Single-Family Housing Price Growth” (with G. Stacy Sirmans, Greg T. Smersh, and Daniel T. Winkler), Journal of Real Estate Research, forthcoming.

Paper overview(2025) “Perceptions of Climate Change and the Pricing of Natural Disaster Risk in Commercial Real Estate” (with G. Stacy Sirmans, Greg T. Smersh, and Daniel T. Winkler), Journal of Real Estate Finance and Economics, forthcoming.

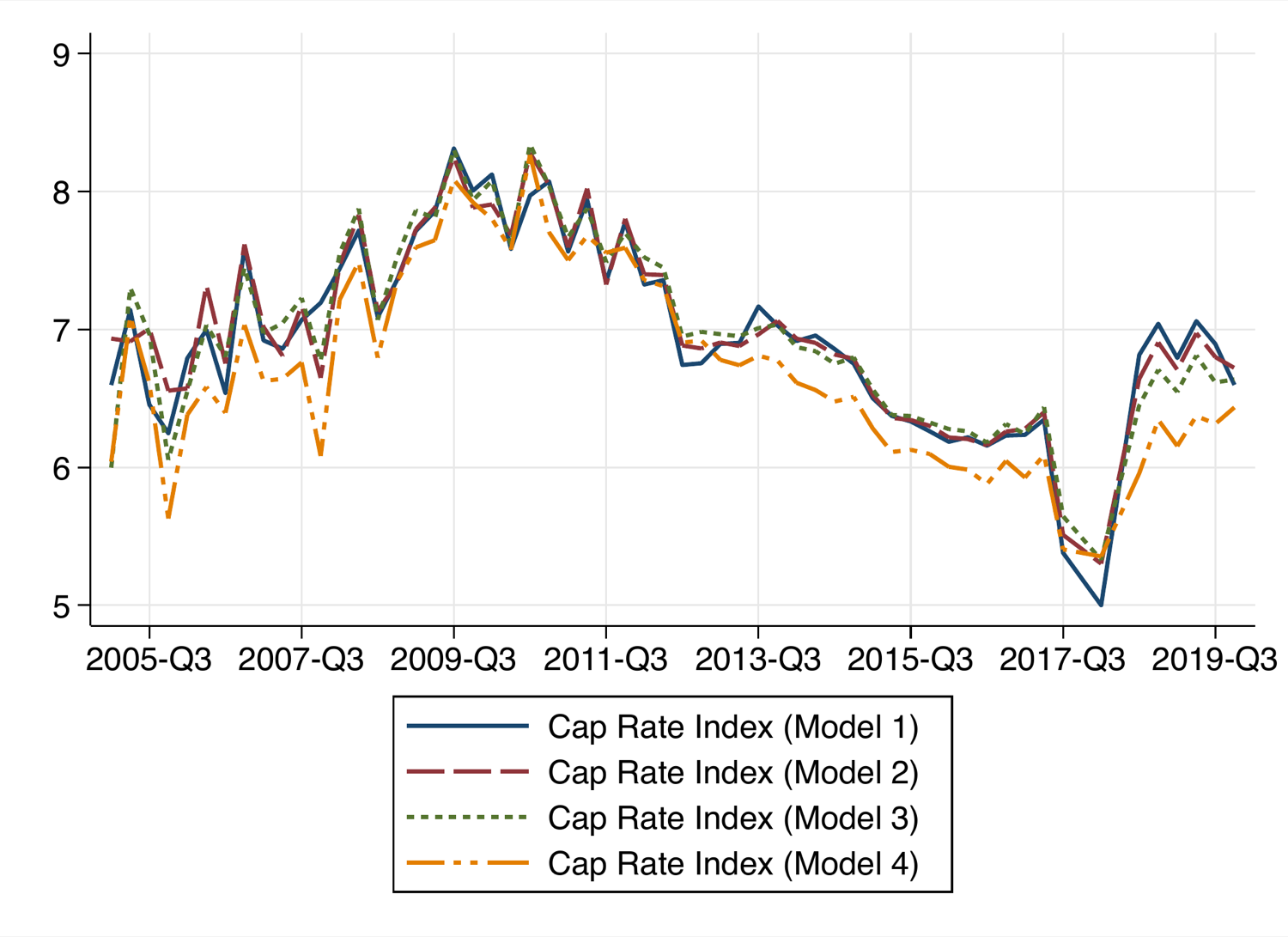

Paper overview(2024) “The Effect of Market Asset Returns, Economic Conditions, and Firm Fundamentals on Net Lease Capitalization Rates” (with G. Stacy Sirmans, Greg T. Smersh, and Daniel T. Winkler), Journal of Real Estate Research, Volume 46, Issue 4, Pages 478-513.

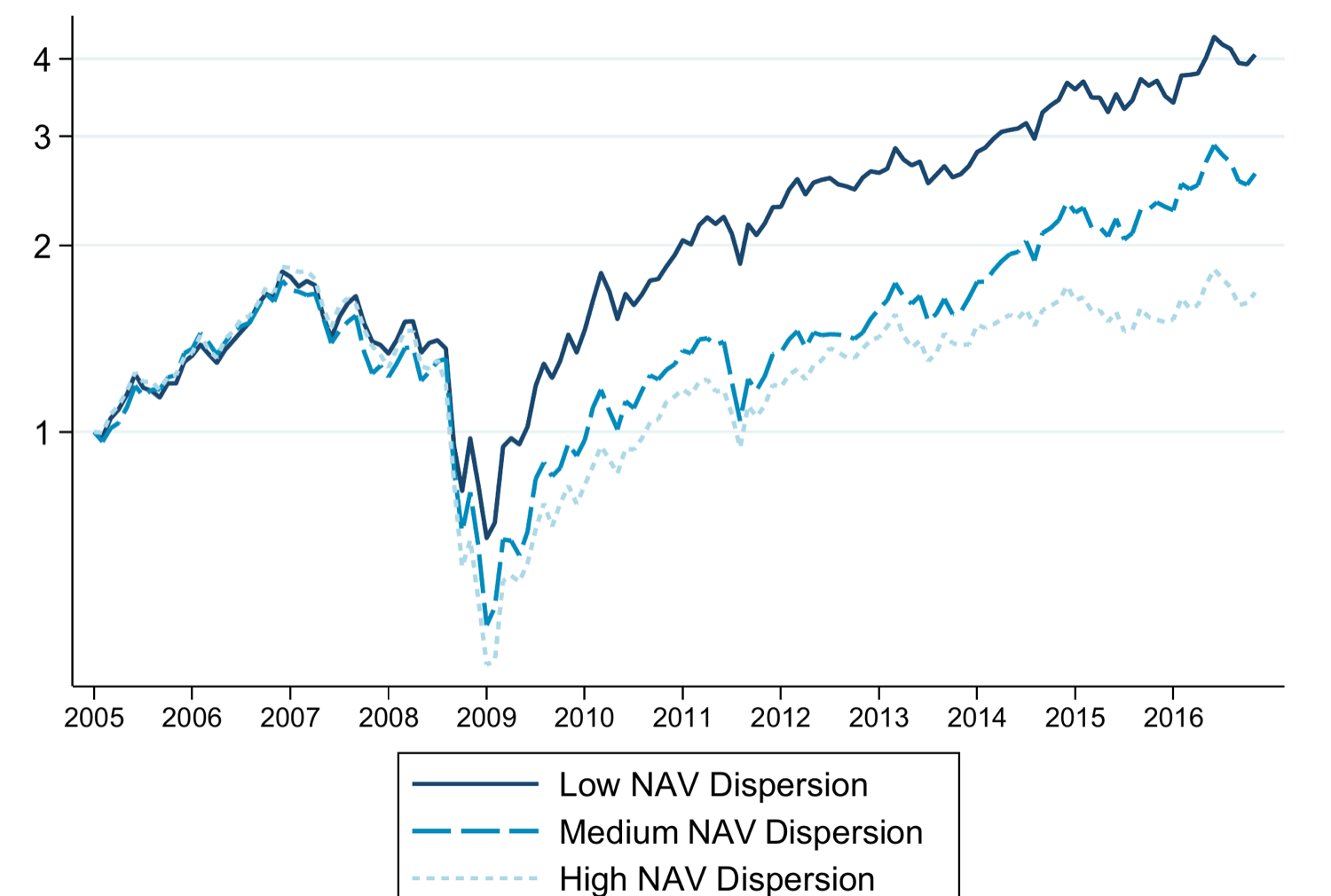

Paper overview(2024) “Spread Too Thin: REIT Asset Dispersion and Divergence of Opinion” (with Mariya Letdin and G. Stacy Sirmans), Journal of Real Estate Finance and Economics, Volume 69, Issue 2, Pages 201-227.

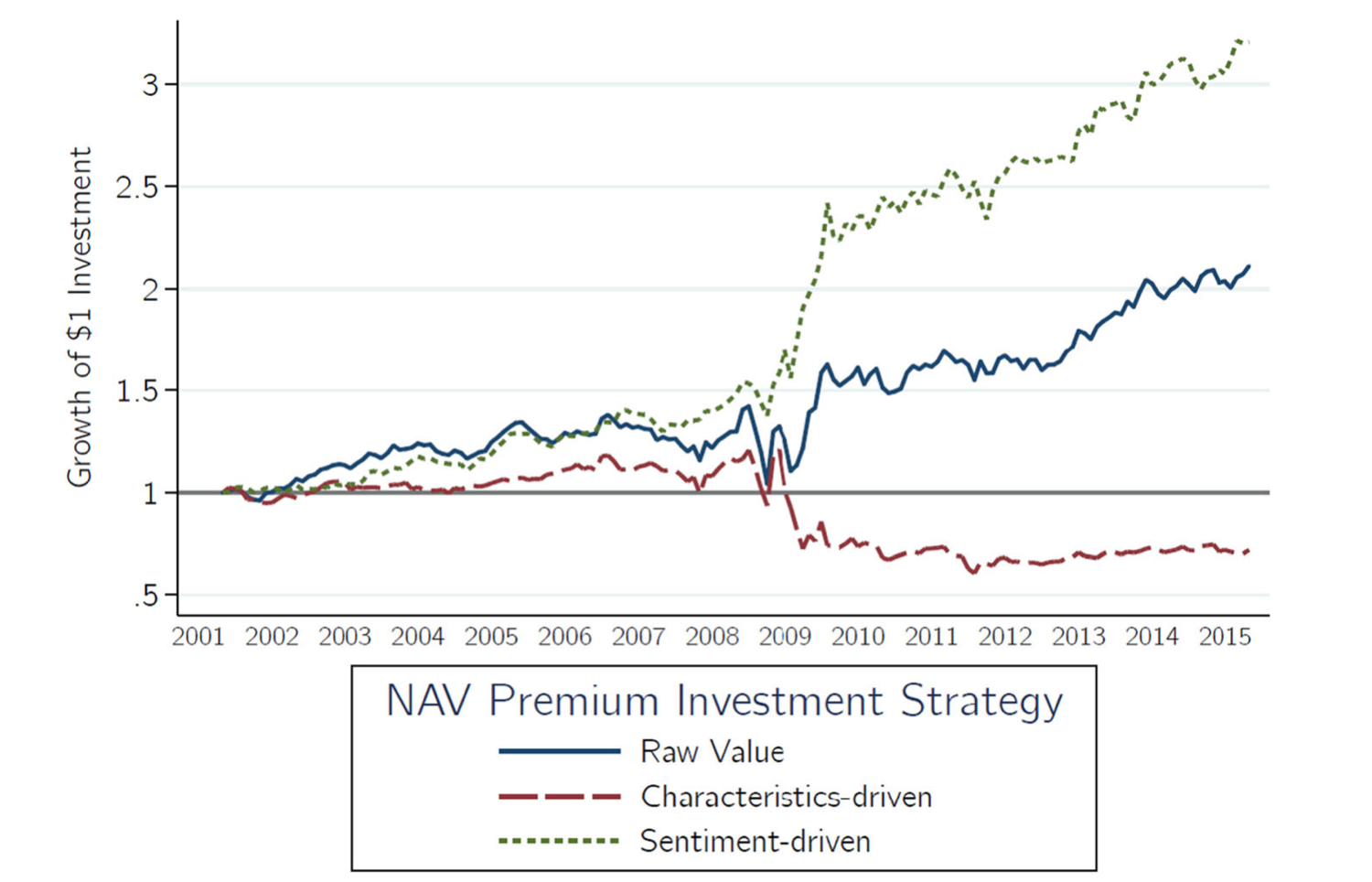

Paper overview(2022) “Betting Against the Sentiment in REIT NAV Premiums” (with Mariya Letdin and G. Stacy Sirmans), Journal of Real Estate Finance and Economics, Volume 64, Issue 4, Pages 590-614.

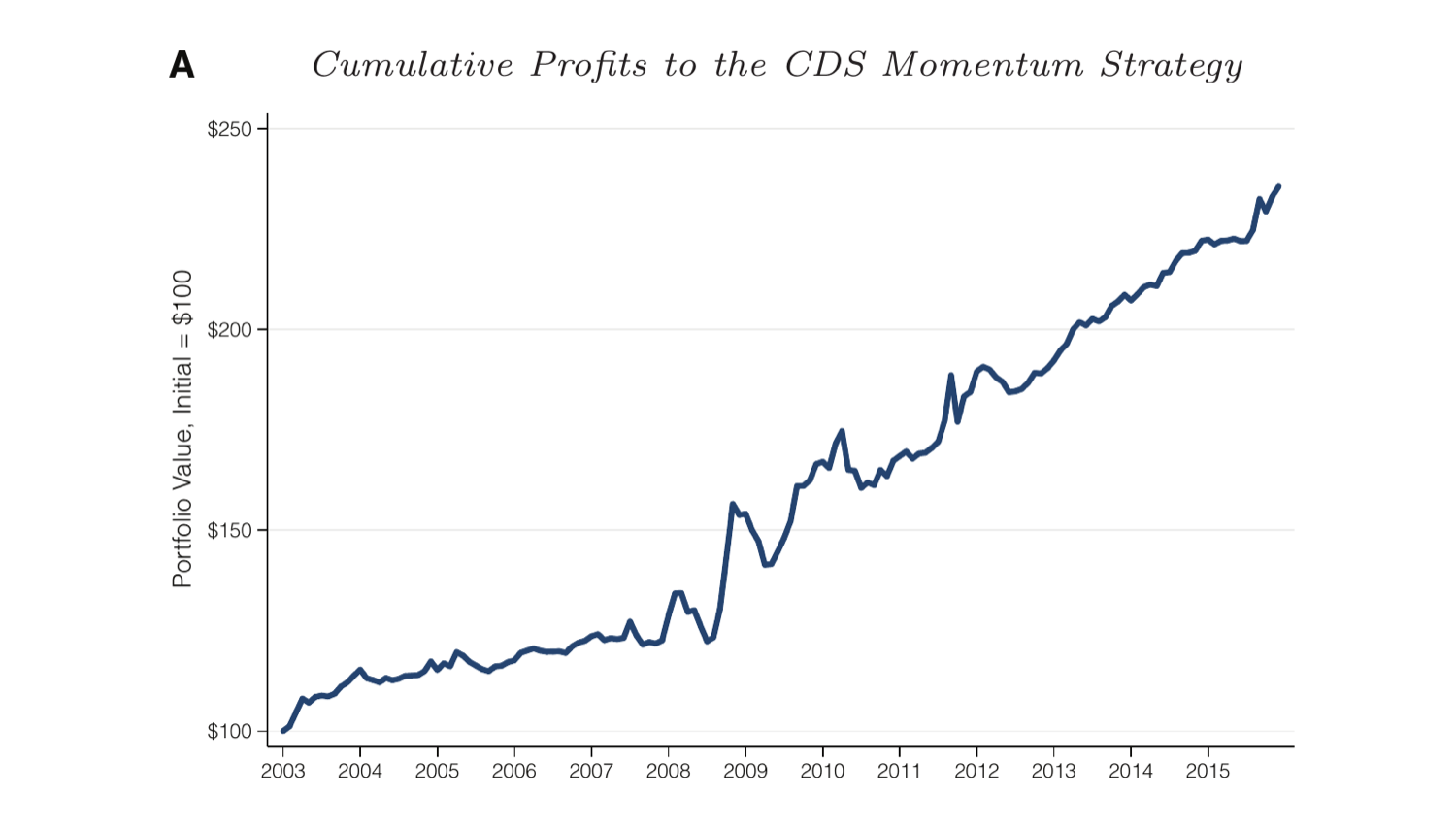

Paper overview(2021) “CDS Momentum: Slow-Moving Credit Ratings and Cross-Market Spillovers” (with Jongsub Lee and Andy Naranjo), Review of Asset Pricing Studies, Volume 11, Issue 2, Pages 352–401.

Paper overview(2019) “Agree to Disagree: NAV Dispersion in REITs” (with Mariya Letdin and G. Stacy Sirmans), Journal of Real Estate Finance and Economics, Volume 71, Pages 10-35.

Paper overview(2019) “Explaining REIT Returns” (with Mariya Letdin, G. Stacy Sirmans, and Emily N. Zietz), Journal of Real Estate Literature, Volume 27, Issue 1, Pages 1-25.

Paper overview(2019) “Observable Agent Effort and Limits to Innovation in Residential Real Estate” (with Justin Benefield and G. Stacy Sirmans), Journal of Real Estate Research, Volume 41, Issue 1, Pages 1-36.

Paper overview(2016) “Exodus from Sovereign Risk: Global Asset and Information Networks in the Pricing of Corporate Credit Risk” (with Jongsub Lee and Andy Naranjo), Journal of Finance, Volume 71, Issue 4, Pages 1813-1856.

online appendixAbstract

Using five-year credit default swap (CDS) spreads on 2,364 companies in 54 countries from 2004 to 2011, we find that firms exposed to stronger property rights through their foreign asset positions (institutional channel) and firms cross-listed on exchanges with stricter disclosure requirements (informational channel) reduce their CDS spreads by 40 bps for a one-standard-deviation increase in their exposure to the two channels. These channels capture effects beyond those associated with firm- and country-level fundamentals. Overall, we find that firm-level global asset and information connections are important mechanisms to delink firms from their sovereign and country risks.Conference Presentations

2013 Southern Finance Association

2013 China International Conference in Finance

2013 WU Gutmann Symposium

2013 SFS Finance Cavalcade(2015) “Determinants of Mortgage Interest Rates: Treasuries versus Swaps” (with G. Stacy Sirmans and Stanley Smith), Journal of Real Estate Finance and Economics, Volume 50, Issue 1, Pages 34-51.

Abstract

The 10-year Treasury rate has long been considered the primary determinant of 30-year mortgage interest rates. The contemporaneous 10-year LIBOR swap rate is shown to better explain the contemporaneous mortgage rate than the contemporaneous 10-year Treasury rate. This result appears to hold over most of the sample period, 1987-2011, using a variety of statistical tests. Given the long-held belief that the mortgage rate is best explained by the 10-year Treasury rate, this paper makes an important contribution to the literature by demonstrating that the swap rate is superior.Conference Presentations

2012 American Real Estate Society(2012) “Property Tax Initiatives in the United States” (with G. Stacy Sirmans), Journal of Housing Research, Volume 21, Issue 1, Pages 1-14.

Abstract

This study reviews the history of property tax initiatives in the United States. Major initiatives include California's Proposition 13, Florida's "Save Our Homes" amendment, and Massachusetts' Proposition 2½. Enacting some type of limitation is most appealing when taxpayers feel overtaxed and underserved. There is some evidence to show that tax and expenditure limitations do bring local governments more in line with voter preferences. Tax limitation initiatives are often funded by vested special interests and are not pure grassroots movements. Studies show that tax limitation initiatives have a negative effect on education through lower teacher salaries and lower student test scores. Studies also show that other public service areas such as fire protection are also negatively affected.

Working Papers and Works in Progress

“The Price of Intelligence: A Hedonic Index for AI Capability” (with Cayman Seagraves).

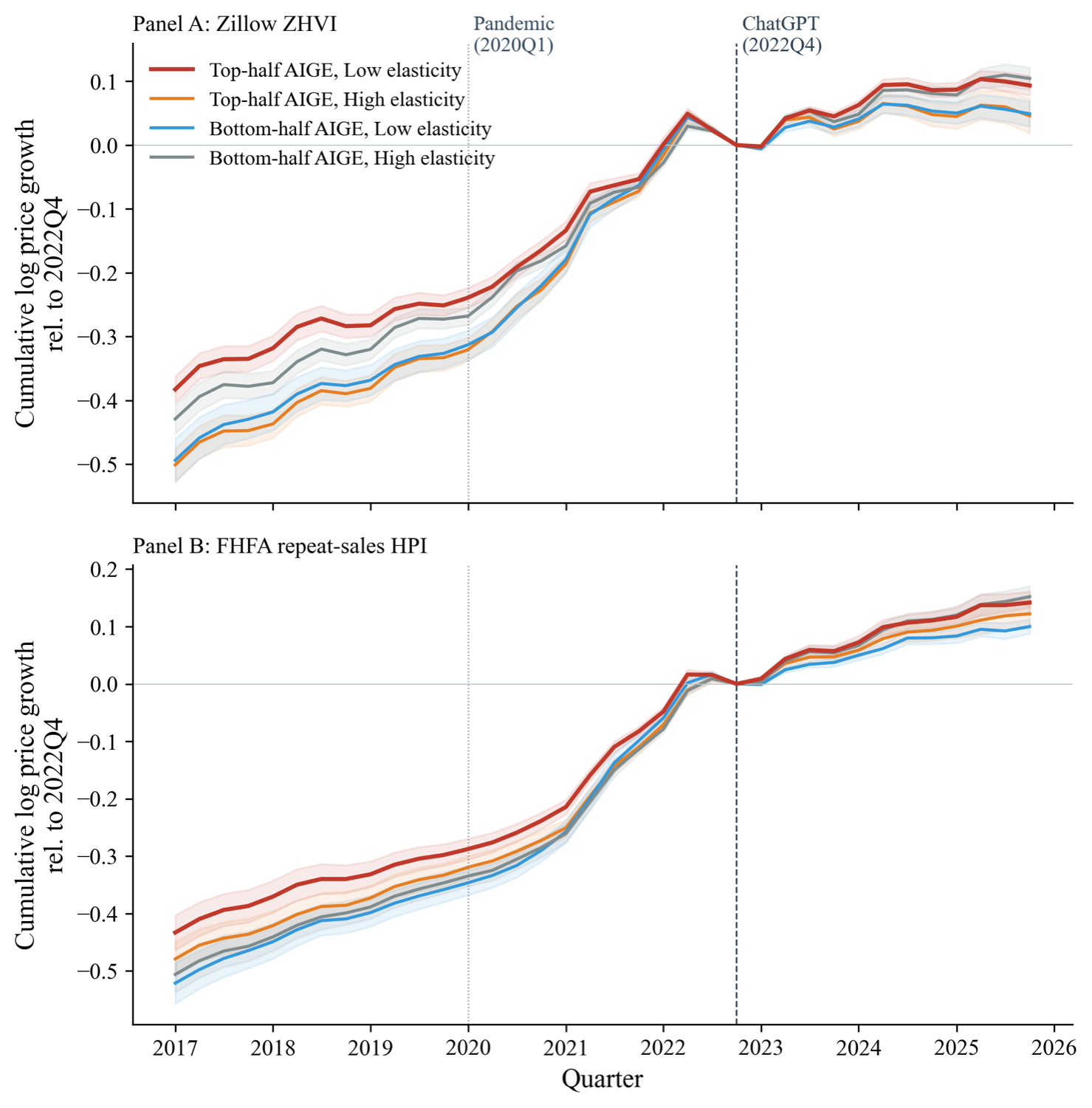

Interactive dashboard“AI Exposure and Housing Markets” (with Cayman Seagraves).

Paper overview“Curvature and Contingencies: Pricing Lease Term Risk in Commercial Real Estate” (with Randy Anderson, G. Stacy Sirmans, and Greg Smersh).

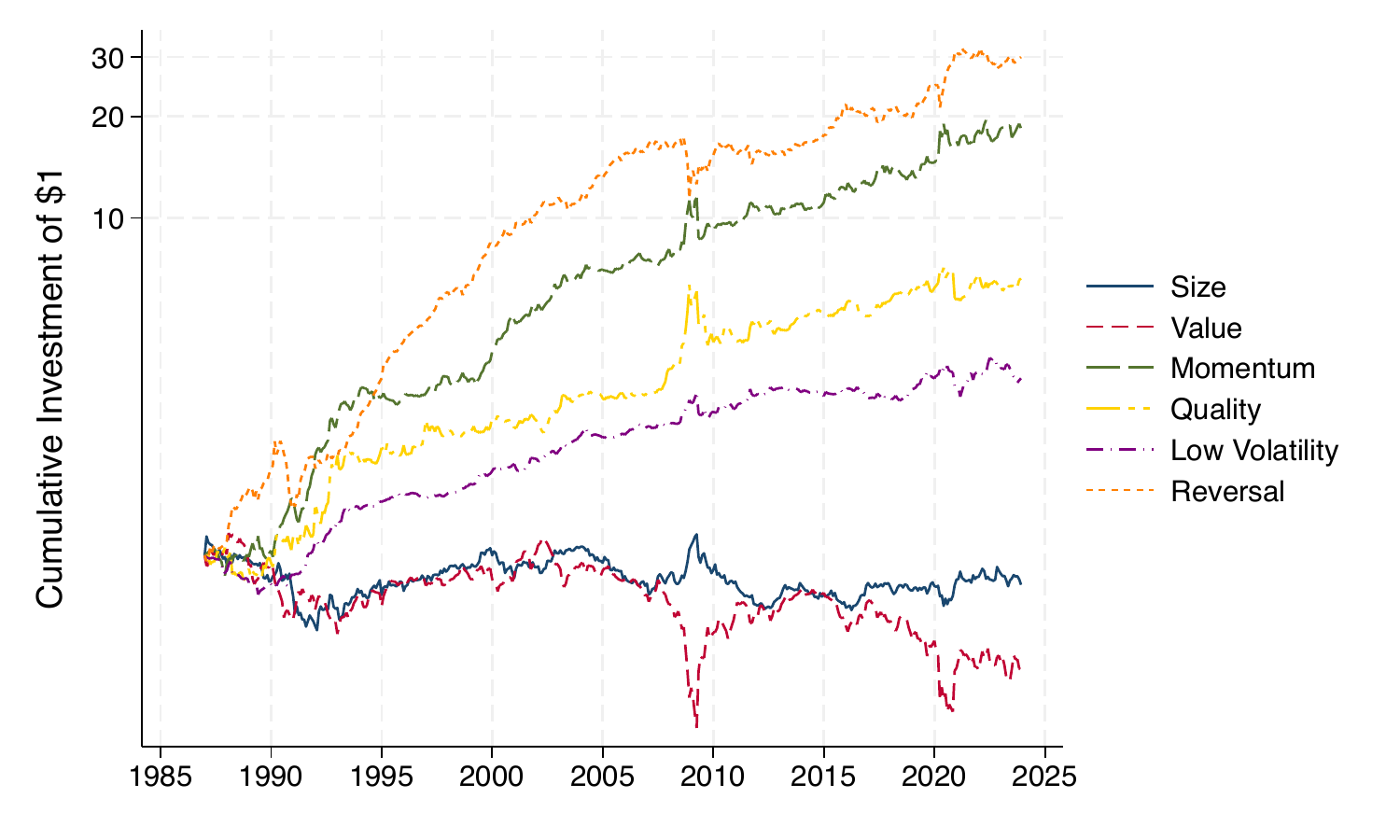

Paper overview“REIT Factors” (with Mariya Letdin and Cayman Seagraves).

Paper overview“Evidence-Based AI for Finance and Real Estate: Retrieval-Augmented Generation” (with Cayman Seagraves).

Corbis“Artificially Biased Intelligence: Does AI Think Like a Human Investor?” (with Javad Keshavarz and Cayman Seagraves).

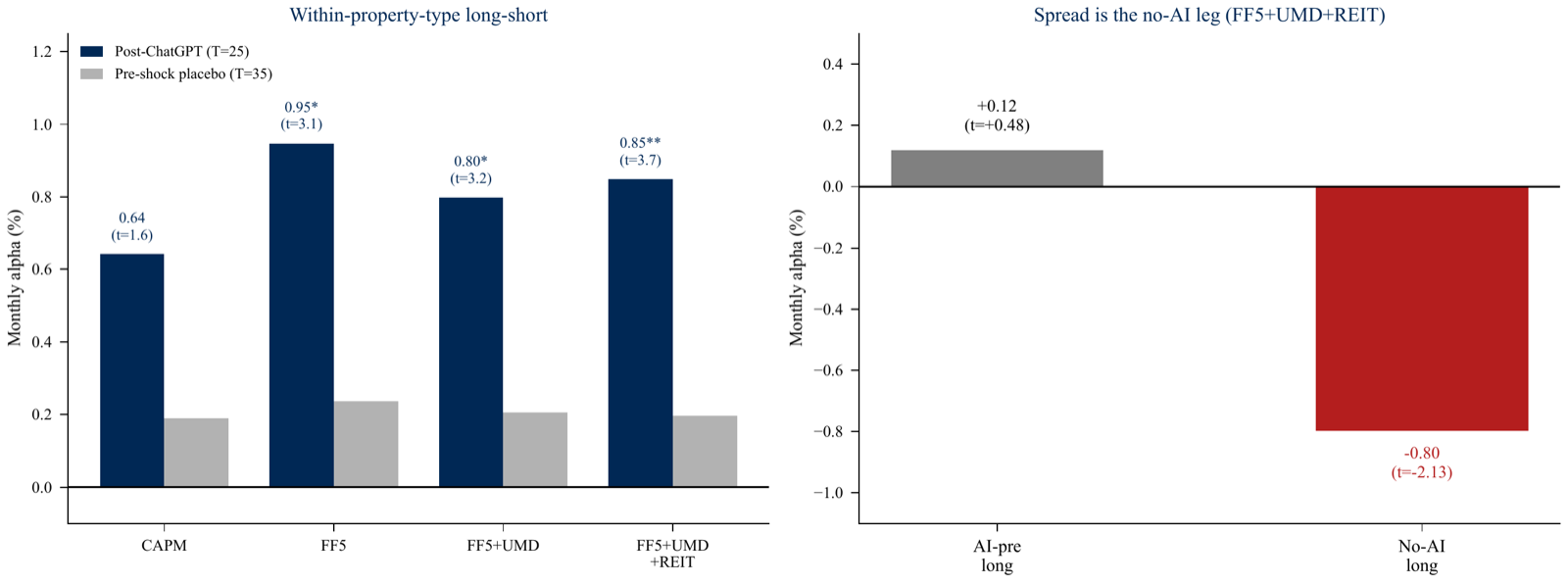

Paper overview“Talk is Cheap, Talent is Expensive: Pricing AI Adoption in Public Real Estate” (with Cayman Seagraves).

Paper overview“Eye in the Sky, Value on the Ground: AI-Derived Visual Cues and CRE Cap Rates” (with Randy Anderson, G. Stacy Sirmans, and Greg Smersh).

Paper overview“Momentum Across the Capital Structure” (with Javad Keshavarz), R&R at the Journal of Financial and Quantitative Analysis.

Paper overview“AI in Residential Real Estate: Efficiency Gains and Equity Gaps” (with Cayman Seagraves and Michael Seiler).

Paper overview“Token Leverage: A Framework for AI Inside the Firm” (with Cayman Seagraves).

Paper overview“Insuring the American Dream: Insurance Affordability and Housing Price Dynamics” (with G. Stacy Sirmans and Daniel Winkler).

Paper overview“The 52-Week High, Downside Risk, and Corporate Bond Returns” (with Javad Keshavarz).

Working Paper

Abstract

We show that the 52-week high stock anomaly is a powerful predictor of corporate bond returns. By anchoring the current price to its 52-week high, the price-to-high (PTH) ratio captures the stock market's most pessimistic view on negative productivity shocks experienced by the firm, disproportionately forecasting adverse events such as earnings surprises and credit rating downgrades. A long-short bond strategy based on the PTH signal yields a monthly alpha of 48 bps, reflecting the gradual incorporation of information into bond prices. The strategy is robust across bond types and markets, exhibits especially strong performance during market downturns, and is distinct from bond momentum, stock momentum spillover, and post-earnings-announcement drift (PEAD) effects. Our findings highlight an important equity-credit interaction, offering insights for investors and researchers into risk and inefficiencies within bond markets.

“Implied Asset Return Profiles, Firm Fundamentals, and Stock Returns” (with Jongsub Lee and Andy Naranjo).

Working Paper

Abstract

We introduce a novel approach to ascertain firms' unobserved asset return distribution implied by the joint pricing of equity and credit securities within a structural framework. Through the modified Merton framework, we propose a two-factor model that captures systematic asset growth and risk-shifting effects on the cross-section of expected stock returns. We show that strong asset returns representing systematic growth options predict higher stock returns, whereas shifting risk from equity to credit forecasts lower stock returns. We also find the performance of many popular stock market factors that overlook the optionality of equity are significantly improved after controlling for asset-level risk-shifting exposure.“Sovereign Overhang and the Integration of Equity and Credit Markets Around the World” (with Jongsub Lee and Andy Naranjo).

Working Paper

Abstract

As governments around the world steadily assume greater financial risk, there is concern about the growing sovereign risk that overhangs the private sector. This paper demonstrates that sovereign risk serves as a unifying factor for the pricing of private sector assets, manifesting through higher R2s in equity and credit returns and stronger synchronicity between asset classes. Widening sovereign CDS spreads signal impending economic policy uncertainty (EPU), diverting investor attention away from firm-specific events and amplifying the role of credit markets in price discovery. Strong property rights protections and rule of law mitigate the dissemination of sovereign risk, while financial institutions and economies with more credit to government entities are especially vulnerable. Our findings provide novel insights into the sovereign-corporate nexus and cross-asset market dynamics, offering implications for global asset pricing and financial stability.

“Related Securities and the Cross-Section of Stock Return Momentum: Evidence from Credit Default Swaps (CDS)” (with Jongsub Lee and Andy Naranjo).

Working paper

Abstract

We document that stock return momentum strategies earn 20% more per year among firms with strong alignment in their past equity and credit returns than firms with diverging returns across these two markets. Using structural Q-theory, we show information in both equity and credit from the full liability side of a firm's balance sheet reveals unobserved asset return momentum that explains cross-sectional variations in stock return momentum. We complement this rationale with limited arbitrage in equity and credit markets to further explain our findings during financial market dislocations. We also show that multi-market related securities signals hedge stock momentum crashes.Conference Presentations

2018 CBOE Conference on Derivatives and Volatility

2017 Numeric Investors

2016 The 14th Paris December Finance Meeting by EUROFIDAI-AFFI-ESSEC

2016 Financial Management Association

2016 Chicago Quantitative Alliance

2016 Northern Finance Association

2016 Financial Econometrics and Empirical Asset Pricing Conference

2016 European Financial Management Association

2016 9th Annual Meeting of the Risk, Banking, and Finance Society

2015 Southern Finance AssociationAwards

2nd Place, 2016 Chicago Quantitative Alliance Academic Competition“The Cost of Diversification in a Market of Specialists” (with Randy Anderson and Julia Freybote).

“Equity to Credit Factor Portability” (with Javad Keshavarz).

Teaching

- AI in Finance: Fall 2026

- Real Estate Capital Markets: Fall 2025, Fall 2026

- Real Estate Investment: Fall 2024

- Principles of Business Finance: Fall 2017, Spring 2018, Fall 2018, Fall 2019, Fall 2020, Fall 2021, Fall 2022, Fall 2023, Fall 2024, Fall 2025, Fall 2026

- PhD Seminar on Financial Markets and Intermediation (co-taught): Spring 2020

- PhD Seminar on Investments: Spring 2017

- International Finance: Spring 2015, Spring 2016, Spring 2017

- Advanced Corporate Finance: Spring 2015

- Debt & Money Markets: Summer 2013